CIO Insight: Watch for more AI‑driven disruption

Markets have been preoccupied with Middle East geopolitics for the last month, but if a ceasefire can be maintained investors are likely to revisit the theme of AI disruption. We believe this theme will be an enduring headwind for markets that may prove more widespread, deeper and more abrupt than currently priced in, compressing margins.

Software, brokers and triple‑B fintech names have been early examples of sectors showing signs of vulnerability. Yet markets have been entering a new phase of identifying sectors vulnerable to automation and disruption, with the scope of possible disintermediation across service sectors potentially larger than anticipated as AI adoption accelerates.

We see other business models that may be vulnerable as we undergo a structural shift driven by AI. Additional service‑oriented areas potentially at risk include managed care, PBMs, investment banking and advertising, in our view. Markets will also differentiate more sharply across issuers based on cash‑flow durability, balance‑sheet flexibility and exposure to margin compression.

As for the implications for credit, while investment grade credit indices have little exposure to software, we do see increasing pressures in sectors with secondary exposures like insurance and BDCs. As we expected, the robust supply calendar, largely owing to the ongoing AI capex boom, has also been a major headwind. Total US hyperscaler issuance has exceeded $80 billion in the first quarter, and overall supply is off to a blistering start.

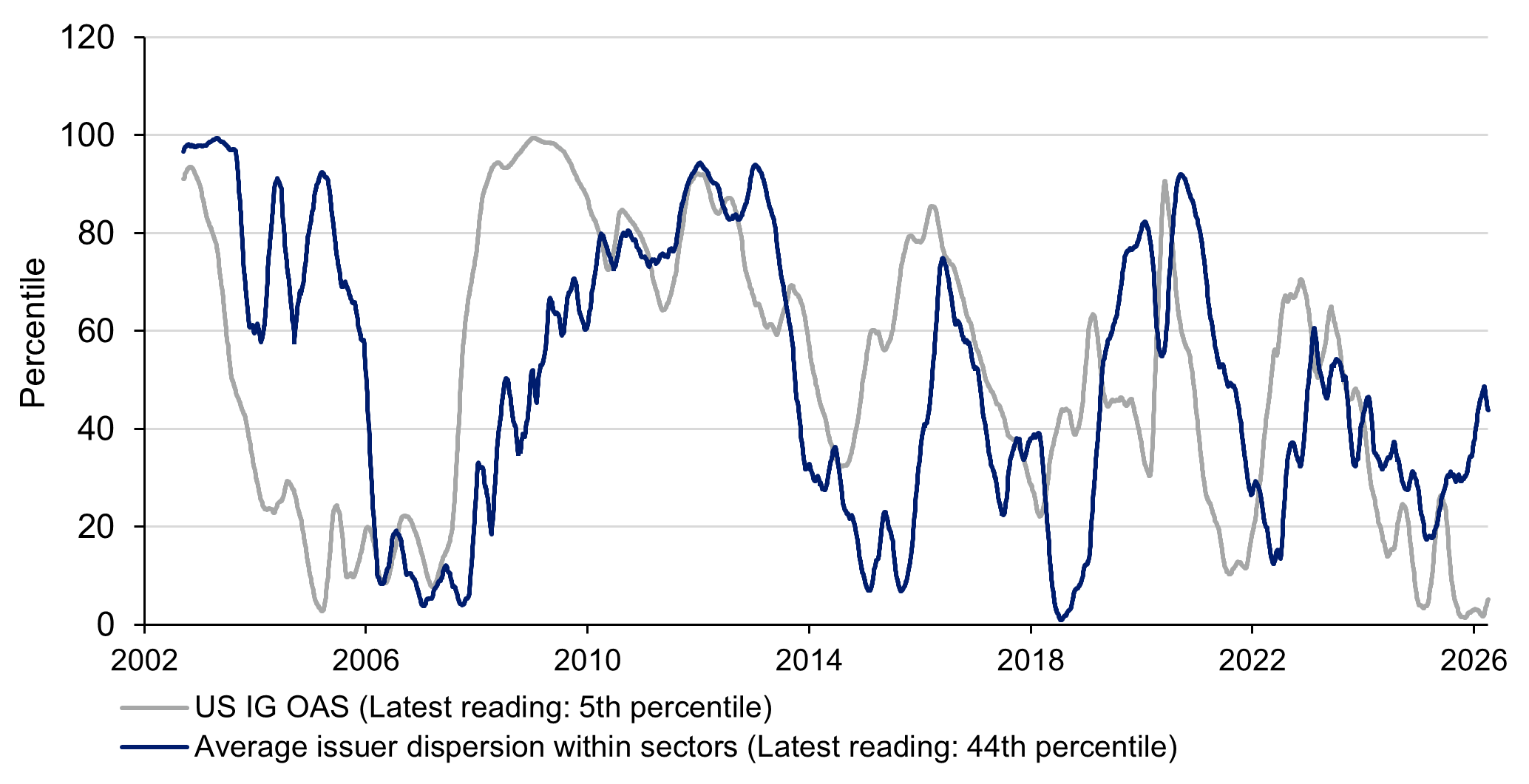

Historically periods of high dispersion among issuers within sectors have aligned with periods of elevated aggregate spreads (Figure 1). Broadly, we expect dispersion to increase above the median (the 50th percentile in Figure 1) amid growing AI disruption, implying that aggregate spreads will rise as well.

We remain relatively cautious given the increasing wall of worry. However, recent new issues have come with generous concessions leaving us more comfortable adding risk through the primary market. Our near-term playbook is to keep risk contained and lean into quality and liquidity. We prefer high quality businesses with hard assets, and we have increased exposure to pharmaceuticals and healthcare in recent weeks.

Figure 1: More dispersion—and higher spreads—likely ahead

US IG vs average issuer dispersion w/in sectors (Percentile ranks over common history, 60d moving avg.)

Source: L&G – Asset Management, America. Data as of April 9, 2026.

Source: L&G – Asset Management, America. Data as of April 9, 2026.

Disclosures

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) and Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. Legal & General Investment Management America, Inc. does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that LGIM America's investment or risk management processes will be successful.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.