CIO Insight: The truth about today’s rising yields

Rates have been on the rise recently, with the 30-year Treasury yield recently reaching its highest level since 2007. Numerous factors are driving the rise in yields, but one truth about the increase is worth highlighting: It has come without the traditional corresponding rise in rate volatility.

Factors driving higher rates included renewed inflationary pressure from elevated energy prices; persistently large government deficits and AI demand requiring ever-increasing bond issuance; the possibility of the Fed remaining on hold for longer with an expressed desire to operate with a smaller balance sheet; and investors demanding higher term premiums and inflation premiums amid deglobalization and increased geopolitical fragmentation.

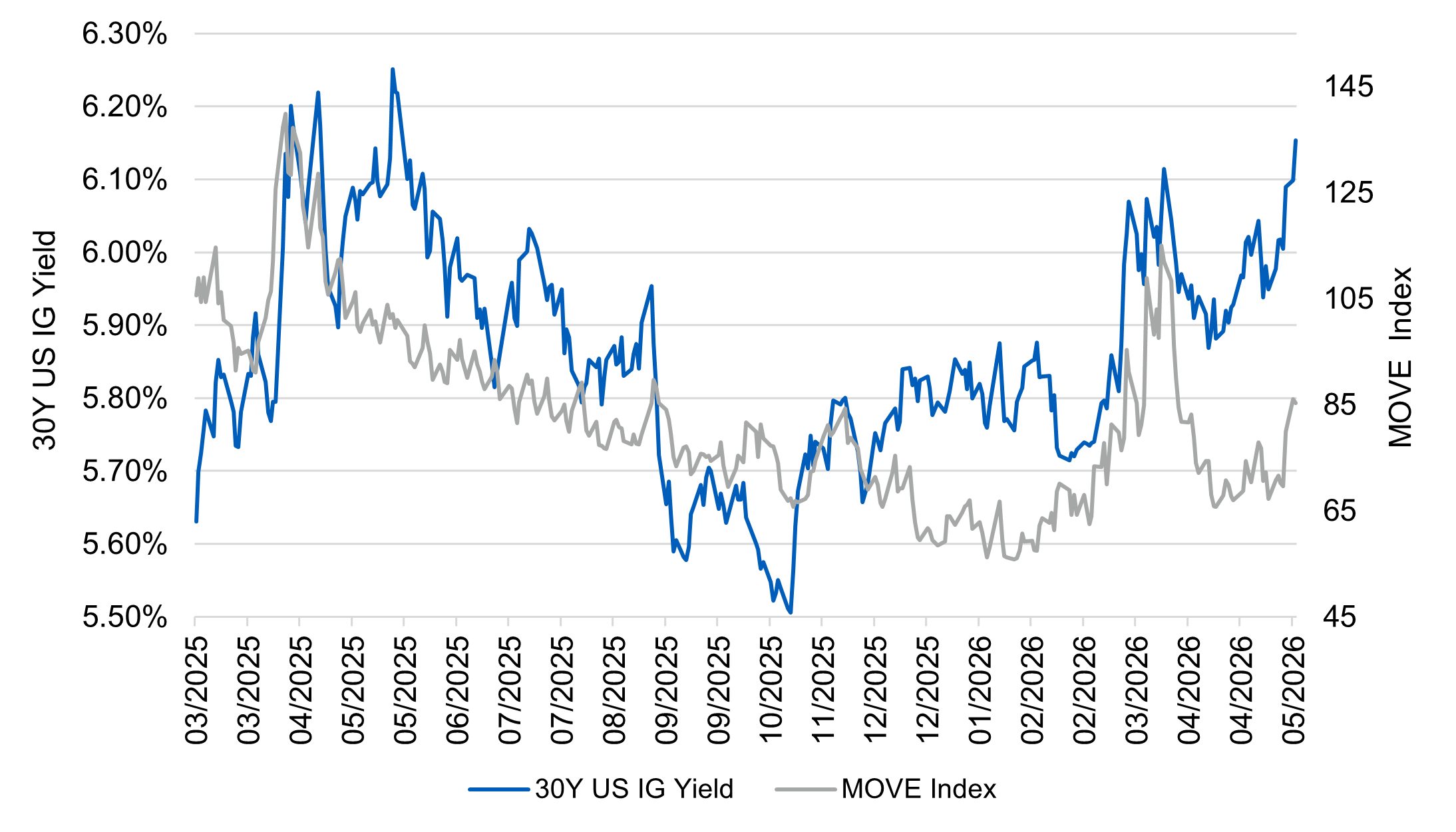

Historically, spikes in rates have coincided with a spike in rate volatility. Today, however, rate volatility still sits near the lower end of where it has been in recent years. This means investors are getting more reward per unit of risk, including in the US credit market. See Figure 1.

In our view, today’s yield backdrop looks more compelling for income than for spread compression. Higher rates continue to support credit technicals, but with spreads tight and the recent rally leaving valuations more demanding, we advocate for discipline and selectivity rather than broadly adding risk—especially where future supply could weigh on performance.

Our view remains neutral on broad credit beta. We see supportive demand and all-in yields, but also a backdrop in which the AI-related capex boom, heavier forward supply and geopolitical uncertainty argue against chasing spreads tighter. We see risks for spreads to go wider should downside risks become more pronounced and/or supply remain robust. Within that setting, we prefer selective positioning, active rotation out of names vulnerable to supply pressure and a focus on capturing value where new issue concessions are available.

Figure 1: Yields climb comes amid historically muted volatility

30Y US IG Yield vs MOVE Index (Since March 1, 2025)

Source: Bloomberg. Data as of May 21, 2026. The MOVE Index (Merrill Lynch Option Volatility Estimate) is a measure of price volatility in US Treasuries.

Source: Bloomberg. Data as of May 21, 2026. The MOVE Index (Merrill Lynch Option Volatility Estimate) is a measure of price volatility in US Treasuries.

Disclosures

Unless otherwise stated, references herein to "L&G" and “L&G – Asset Management” refer to the global asset management business of Legal & General Group plc. that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser), Legal & General Investment Management Japan KK (licensed by the FAS in Japan), and LGIM Singapore Pte. Ltd. (licensed by the MAS in Singapore). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. L&G – Asset Management, America does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that L&G – Asset Management, America’s investment or risk management processes will be successful.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.