The case for US multifamily commercial real estate

Investors choosing to diversify their portfolios with US property have a wide array of property types on offer. However, there is one subsector that we believe is especially attractive in today’s investment environment: US multifamily.

Multifamily investments have delivered essentially the same degree of portfolio diversification as US commercial real estate (CRE) as a whole in recent years, while also outperforming the broader US CRE market. Looking forward, we see this trend continuing amid favorable demand-and-supply dynamics, though the investment performance outlook for multifamily is not uniform across US metro areas and selectivity is key for capturing this opportunity.

A track record of outperformance

Multifamily investments are a subsector of the NCREIF “residential” sector called “apartments.” The subsector has provided roughly the same diversification benefit as the whole universe of US institutionally owned properties, as evident in the high correlation (0.97 for 1-year total returns over 2000-2025) between the NCREIF Apartment Index and the total NCREIF-Expanded NPI benchmarks.

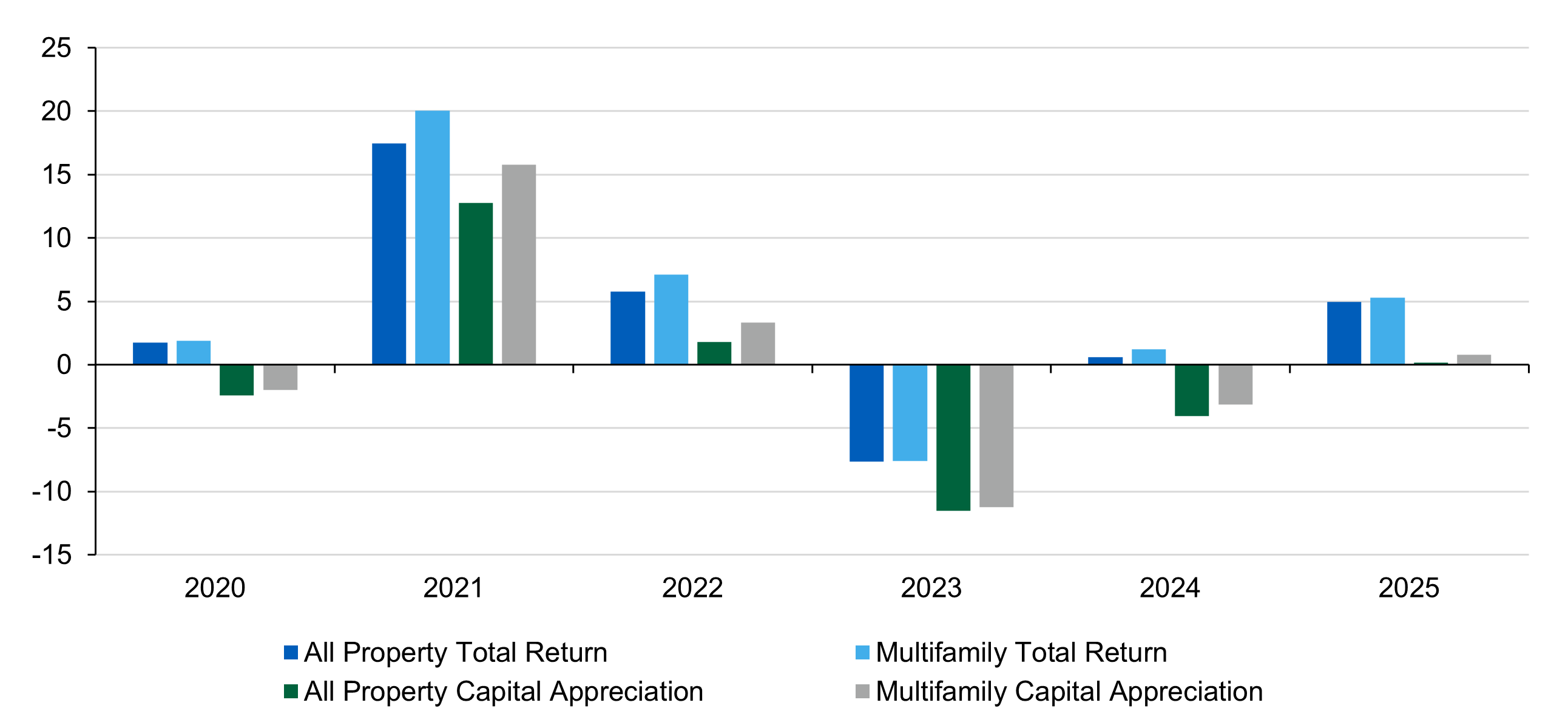

In addition to offering this diversification benefit, the multifamily sector has outperformed the broader NCREIF universe in the six years since COVID emerged in 2020. As shown in Figure 1, multifamily has outperformed annually beginning in 2020, both in total return and in the capital appreciation component of total return.

Figure 1: Multifamily has outperformed

Source: NCREIF

We attribute the superior performance of multifamily during this challenging period to the characteristics of US multifamily demand and supply, characteristics that we believe are likely to persist in supporting strong performance over the period ahead.

Demand: Gen Z population cohort is enormous

Younger millennials who are still renters and the maturing Gen-Z generation are fueling demand for apartments in multifamily properties. The Gen Z generation was born between 1997 and 2012, with the oldest now 29 and the youngest 14. Gen Z follows the much-touted millennial generation, which is the largest since the Baby Boom. The Gen Z cohort is 88% as large as the millennial generation.

The oldest Gen Zers (those 25-29 years old in 2023) are predominantly renters, according to the latest census data collected in 2023; only 30% were homeowners. A hefty 54% of younger millennials (those 30-34 years old) were also renters in the 2023 data. Homeownership for older millennials (those 35-44 years old) was closer to the norm at 61%.

The high propensity of renting among older Gen Zers and younger millennials suggests that maturing Gen Zers will continue to boost demand for apartments. Moreover, we believe there is hidden demand in the 23% of older Gen Zers and 12% of younger millennials who still live with their parents. These metrics reflect the difficulty of attaining homeownership today. This is unlikely to change in the years ahead, supporting our assumption that ongoing demand for apartments is solid.

Supply: Housing shortage continues

In a July 2025 widely quoted report, using updated Census data, Zillow estimated a 4.7 million shortfall in US housing units. The shortage can be traced to the drop in housing construction in the aftermath of the 2008 Great Recession combined with the maturation of the enormous millennial population cohort born between 1981 and 1996.

The oldest millennials were 27 in 2008, an age commonly characterized by finishing education, beginning careers and renting apartments. To accommodate maturing millennials, older households would have typically been moving out of apartments into single-family homes. The aftermath of the recession curtailed that transition, as single-family construction plummeted and access to home purchasing tightened. Between 2000 and 2007, single-family housing starts averaged 1.4 million per year; between 2008 and 2019, the average was 656,000.

The shrinkage in new supply pushed up home prices by 41% between the end of the recession in 2009 and 2019. Surging home demand during the COVID pandemic and historically low mortgage rates further propelled the sharp run-up in home prices. Home purchases soared in 2022, pushing prices up another 56% and making ownership even more out of reach. With single-family homes out of reach, millennial households increasingly remained as apartment renters. Multifamily property construction did increase modestly in 2022-2023 but not nearly enough to make up for the single-family shortfall.

As maturing Gen Zers added to apartment demand in the aftermath of the COVID lockdowns, rent growth accelerated. Between 2019 and 2025, the average rent for institutional quality apartments increased 2.9% per year. This pace exceeds the 1.9% per year increases between 2009 and 2019 and is contributing to US inflation. At the same time, it is a benefit to investors.

Metro area performances differ widely

Solid demographic demand and limited potential for homeownership bode well for ongoing attractive rent growth for institutional quality multifamily investments, but multifamiliy performance prospects differ across US metro markets.

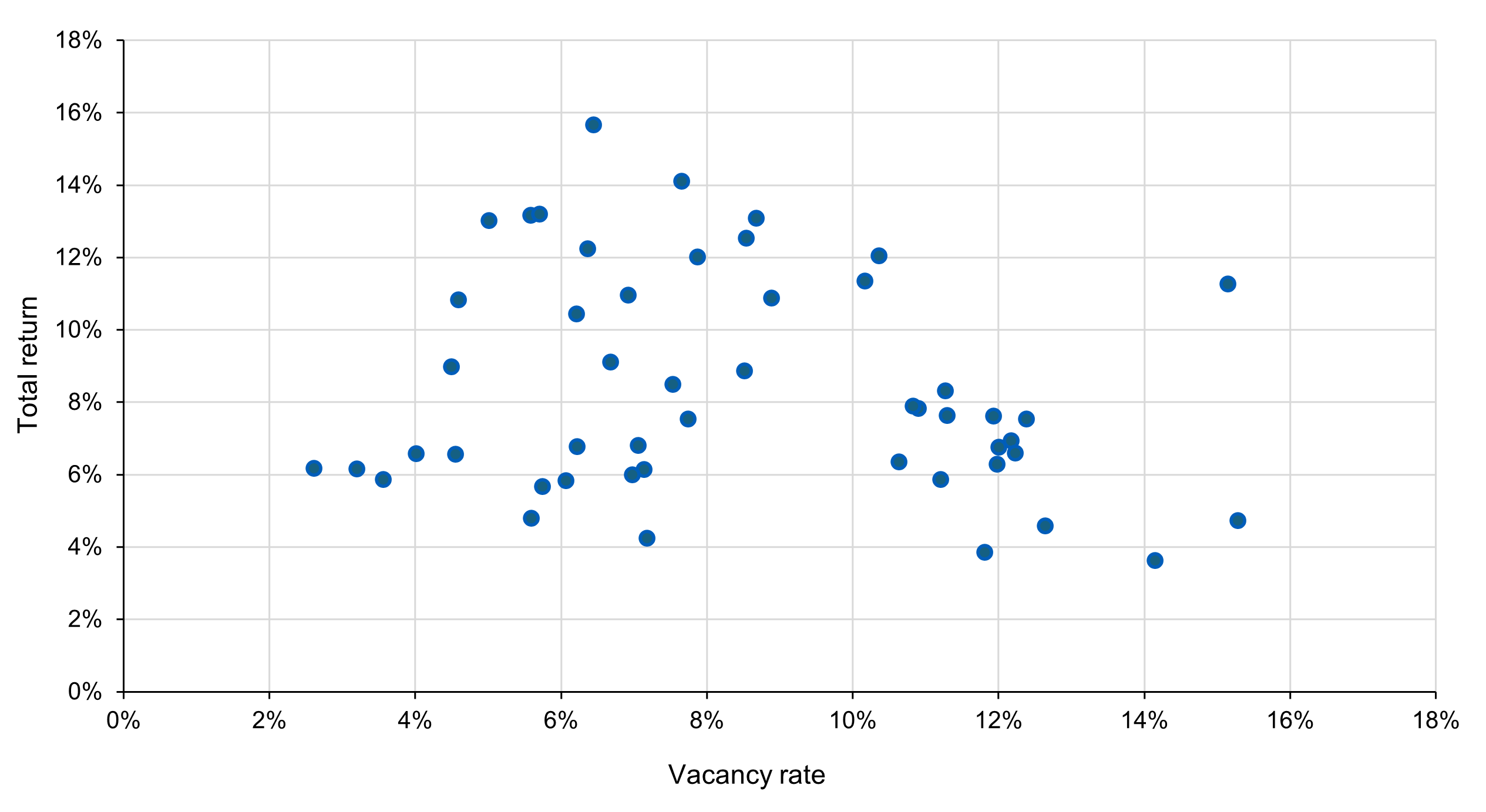

The wide dispersion in multifamily performance by metro area is illustrated in Figure 2, which shows 2025 apartment vacancy rates and total return performance for the top 50 metros ranked by the number of institutional quality apartment units.

As shown, 2025 vacancy rates range from a low of 2.6% to a high of 15.3% across metro areas. Total return performance for 2025 is negatively related to vacancy rates but also reflects a variety of other factors influencing the demand for apartments. Total return for 2025 ranged from 15.7% to 3.6%. Metro investment performance for the longer term 2020-2025 period is positively correlated with 2025 performance but not perfectly aligned. The range for the longer-term metric is 1.4% to 13%.

Figure 2: There is a wide dispersion in multifamily performance by metro area

Top 50 metros-apartment total return & vacancy rate (2025) Source: Costar.

Source: Costar.

The investing implications

Capturing the potential opportunity in multifamily investing requires evaluating metro areas for the factors that influence vacancy rates and historical total return performance. Demographics are important, with metros attracting inflows of educated young people preferable. That attraction depends on the availability of plentiful job opportunities generated by businesses that are prospering in the region.

For multifamily investors, metros with expensive single-family housing may lock-in apartment tenants and contribute to relatively stronger rent growth potential. Constraints on construction of apartments via zoning or limited site availability are also favorable for investors. Other considerations include climate-related risks and the cost of insurance. Finally, the timing of acquisitions and dispositions matters and requires tracking local market conditions closely over time.

The bottom line: We believe US multifamily properties in attractive metros are still a good bet.

Disclosures

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) and Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. Legal & General Investment Management America, Inc. does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that LGIM America's investment or risk management processes will be successful.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.