The case for listed infrastructure

Infrastructure is the system of networks and services that keep the global economy functioning—water and gas utilities, energy transport and distribution, communications towers, airports and toll roads. These assets stand out as a stabilizing force in institutional portfolios. Their revenues are typically anchored by high barriers to entry, regulation, long‑term contracts and essential demand, creating predictable inflation‑linked cash flows that display resiliency through a wide range of economic conditions, even during recessions or market shocks.

Infrastructure exposure is often associated with private (unlisted) funds that own assets directly. But listed infrastructure—the equities of publicly traded companies that own and operate similar essential, long-lived assets—can be an effective complement to private exposures, in our view. We believe the case for listed infrastructure as a complement rests on predictable cash flows, diversification and liquidity.

Predictable cash flows

Many investors are drawn to private infrastructure assets for their predictable, stable cash flows. Yet the cash flows of listed infrastructure have these characteristics as well, as they result from the fundamental nature of infrastructure assets overall, whether listed or unlisted.

Infrastructure businesses in general typically have regulated returns (where a regulator influences allowable revenues and returns on invested capital), long-term contracted revenues, or other arrangements that reduce sensitivity to short-term swings in demand and limit competition. Demand for infrastructure’s essential services also tends to be inelastic and more persistent than demand for many cyclical goods. These structures and features don’t eliminate risk, but they can help make cash flows more predictable and less reliant on the economic cycle.

In addition, many infrastructure operators have ongoing opportunities to reinvest—for example, by expanding networks, upgrading assets or connecting new customers. Over time, the mix of durable cash generation and reinvestment can lead to stable, long-term returns.

For investors, listed infrastructure can offer transparency into these characteristics as well as access to infrastructure assets that may not be available in private markets. Listed markets are the main way to access US regulated utilities, for instance.

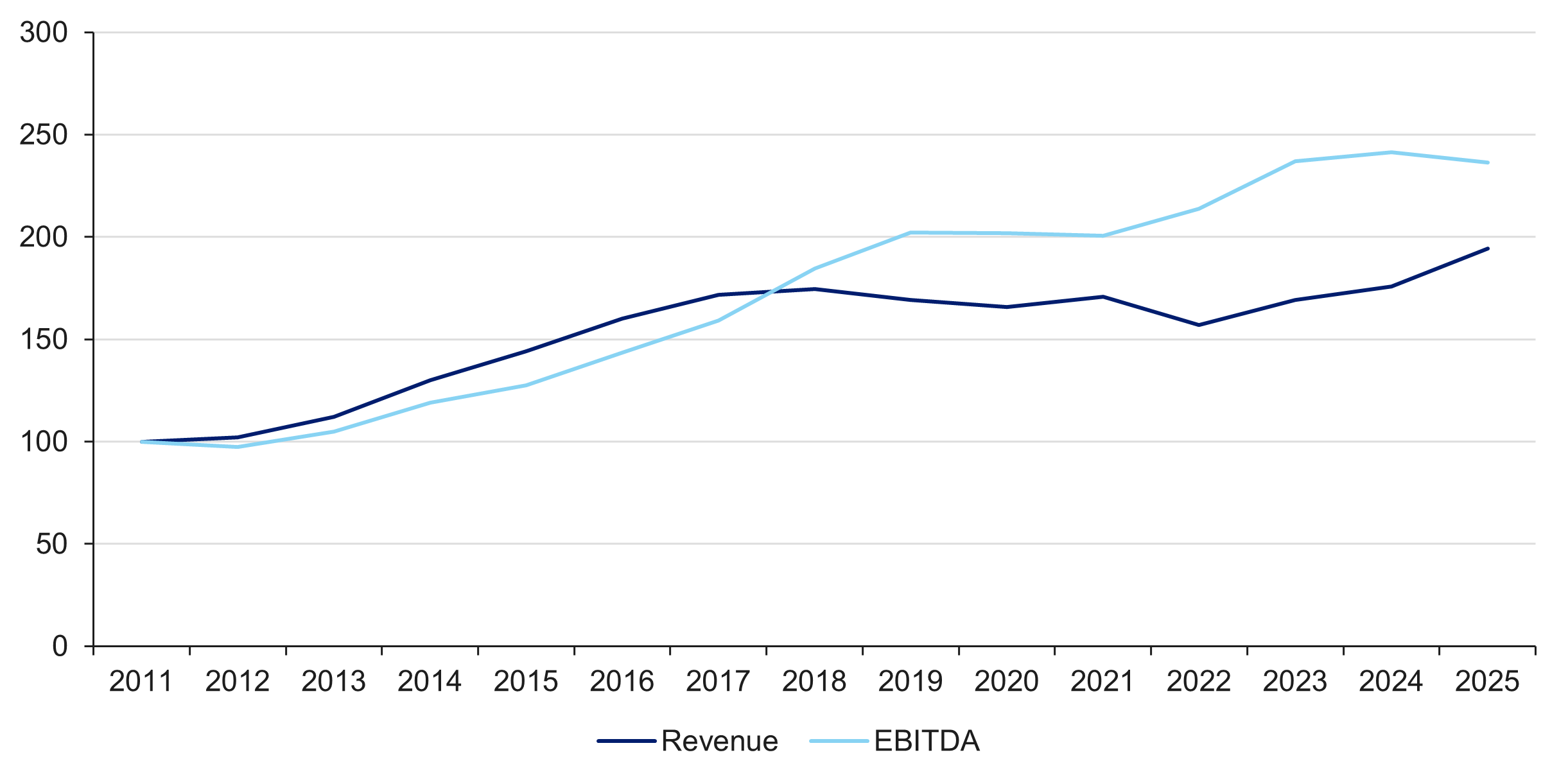

Take TC Energy, a listed energy infrastructure company that operates a large portion of North America’s gas transportation backbone. It offers unusually high cash-flow visibility, given its contract structure and regulated frameworks, with 98% of its earnings before interest, taxes, depreciation, and amortization (EBITDA) underpinned by rate-regulated or long-term take-or-pay contracts. Figure 1 illustrates its predictable cash flows and earnings growth.

Figure 1: Listed infrastructure assets can provide predictable cash flows and earnings growth

TC Energy - Indexed at 100  Source: Bloomberg. Data reflect the time period 2011-2025.

Source: Bloomberg. Data reflect the time period 2011-2025.

Diversification

Listed infrastructure can offer diversification within the infrastructure asset class, providing access to subsectors, such as regulated utilities, and regions not widely accessible in private markets. It also can provide diversification to a portfolio in general, because its drivers of revenue and risk can differ from those of traditional equities and credit.

Case in point: Listed infrastructure’s rolling correlation to US equities is roughly in line over the last 10 years with that of both emerging markets and REITs, other asset classes often viewed as portfolio diversifiers (Figure 2).

Figure 2: Listed infrastructure can offer diversification benefits similar to EM equities and REITs

Rolling 3-year correlation to US equities

Source: Bloomberg. Data as of December 31, 2025. Listed infrastructure is represented by the S&P Global Infrastructure Index, REITs by the S&P US REIT Index and emerging markets by the MSCI Emerging Markets Index. Net return indices are used. Correlations are measured against US Equities, represented by the S&P 500 Index.

Source: Bloomberg. Data as of December 31, 2025. Listed infrastructure is represented by the S&P Global Infrastructure Index, REITs by the S&P US REIT Index and emerging markets by the MSCI Emerging Markets Index. Net return indices are used. Correlations are measured against US Equities, represented by the S&P 500 Index.

Private infrastructure is often viewed as offering attractive portfolio diversification benefits, relative to both the broader equity market and to listed infrastructure. An important feature of unlisted infrastructure, however, is the valuation methodology used for private assets. It is appraisal-based and often computed with a lag of several months. This smooths out returns and dampens correlations, especially versus listed infrastructure markets that reflect real time pricing.

Investors thus should be mindful that listed and private infrastructure can appear different in the short run. Listed markets provide continuous price discovery, so volatility can look higher even when operating performance is steady. From a portfolio construction perspective, that transparency can still be valuable: It can make risks visible earlier and support disciplined rebalancing.

Liquidity

Liquidity is perhaps the most important differentiator between public and private infrastructure. Listed infrastructure can be bought and sold on an exchange, making it easier to change position sizes, meet cash needs or rebalance when markets move. That flexibility matters for real-world implementation. With the help of listed infrastructure, investors in unlisted infrastructure can potentially maintain target exposures, respond to evolving objectives, and reduce reliance on the timing of capital calls and distributions in private funds.

For investors who allocate to both, listed infrastructure can serve as a liquid sleeve alongside private holdings—helping keep infrastructure exposure in place while private assets are being sourced, acquired or realized. It can support commitment pacing and reduce the “cash drag” that can arise when capital is raised for private deployments over time. Put differently, listed infrastructure’s liquidity doesn’t just offer convenience; it can improve the efficiency and resilience of an overall infrastructure program.

Concluding thoughts

Listed and unlisted infrastructure are not mutually exclusive. Private infrastructure may provide access to specific assets and long-duration ownership structures, while listed infrastructure can provide daily liquidity and transparent pricing that can help investors implement, rebalance and manage an overall infrastructure allocation through market cycles. When used together with private infrastructure, listed infrastructure can help investors pursue stable returns, strengthen diversification and manage exposures more effectively through market cycles.

Disclosures

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) and Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. Legal & General Investment Management America, Inc. does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that LGIM America's investment or risk management processes will be successful.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.