The worst of times; the best of times? Private markets react to an uncertain world

Private markets exhibit resiliency amid global shocks. In this blog, we examine trends, key risks, and sector‑specific levers shaping these asset classes in 2026 to-date.

Private markets entered 2026 facing an unusually complex mix of forces: geopolitical tensions, lingering inflation pressures and rapid technological disruption driven by artificial intelligence (AI). Despite this challenging backdrop, the underlying data suggests private assets are in a position of relative strength.

Amid uncertainty, fundamentals across private credit, infrastructure and real estate remain broadly intact. In our view, the key question for investors is not whether risks exist—they clearly do—but how each asset class absorbs and responds to them. Selectivity and resilience are as important as ever with dispersion across sectors, regions and strategies intensifying.

Private credit: Strength beyond the headlines

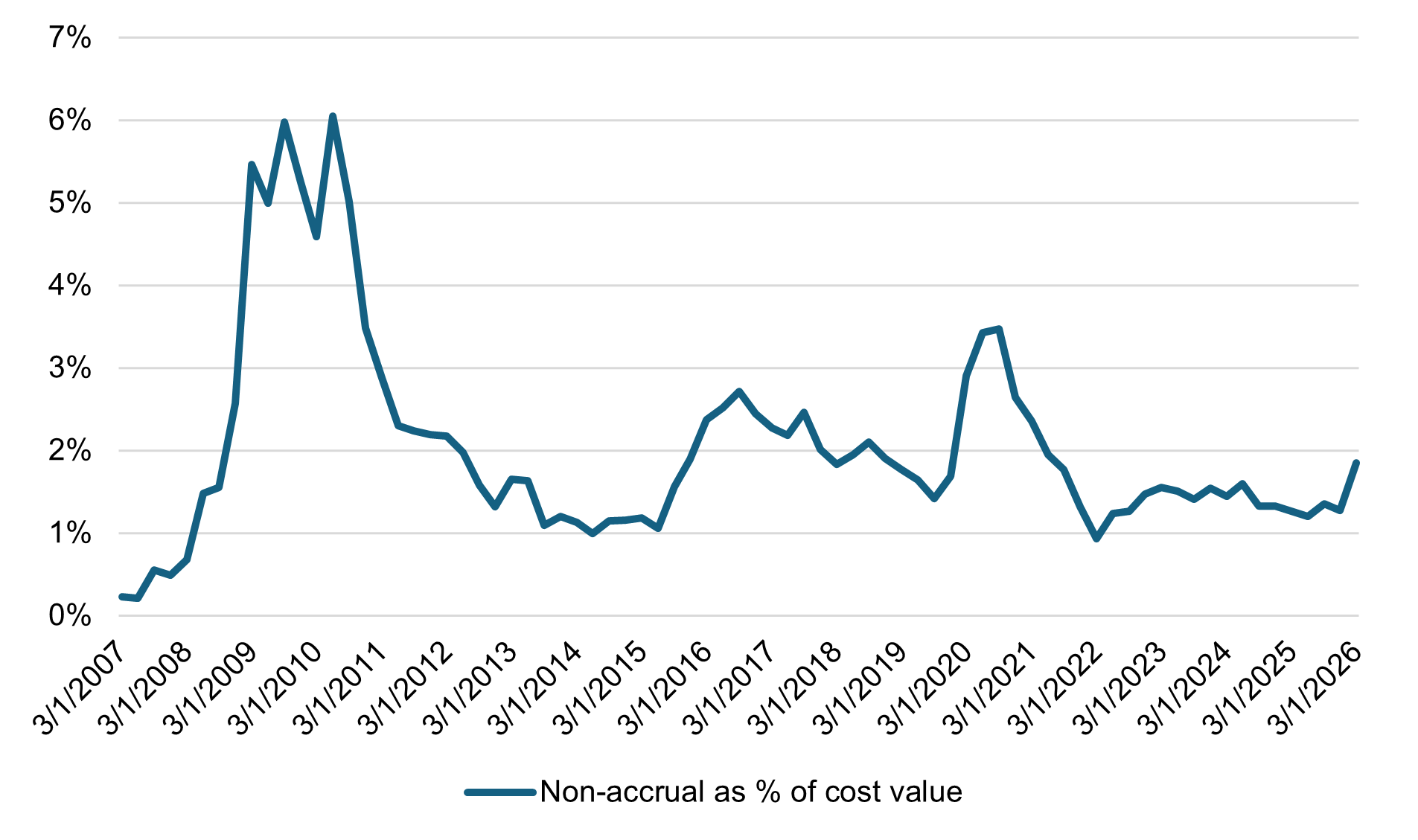

Despite persistent negative headlines, private credit continues to show a largely benign risk picture. Data through the first quarter of 2026 indicated that default and payment‑in‑kind (PIK) rates remained broadly rangebound for sub-investment grade (sub-IG) private credit.1

This stability matters because expectations of future deterioration are rising. AI‑driven disruption poses clear risks to certain business models, while a potential second wave of stagflation could weigh on corporate cash flows. However, starting conditions are comparatively healthy. We believe any deterioration will be manageable rather than systemic.

Market dynamics are also shifting. Yields have risen, spreads are finally expanding after years of compression and lending terms have become more favorable to creditors, reflecting a more cautious borrower environment.

Figure 1: Direct lending default rate

Source: Cliffwater. Data as of May 2026.

Source: Cliffwater. Data as of May 2026.

This doesn’t mean there aren’t areas that warrant close monitoring. Business development companies (BDCs), for example, have experienced a rise in net outflows,2 which could impact these vehicles' liquidity and long-term performance if redemption requests remain elevated in the coming months.

As such, we continue to favor resilience within private credit allocations. Underwriting discipline and risk management will determine how portfolios navigate this period of uncertainty.

Infrastructure: Normalization, not weakness

Infrastructure can be said to sit at the center of the geopolitical and macroeconomic debate. While fundraising and transaction volumes slowed in the first quarter of 2026,3 this followed an unusually strong end to 2025. In our view, this suggests normalization rather than the start of a downturn.

Return dispersion across sectors is now particularly pronounced in Europe, the Middle East and Africa (EMEA) infrastructure markets.4 This suggests that sector-specific forces are increasingly driving returns for European infrastructure and highlights the growing importance of more strategic sector allocations beyond diversified portfolios for additional returns.

Considering the conflict in the Middle East, we believe energy and utilities assets could prove more defensive in a potentially higher‑inflation regime, while volume‑sensitive transport assets are more exposed to demand slowdowns. Additionally, the conflict has also reinforced the strategic importance of energy security.

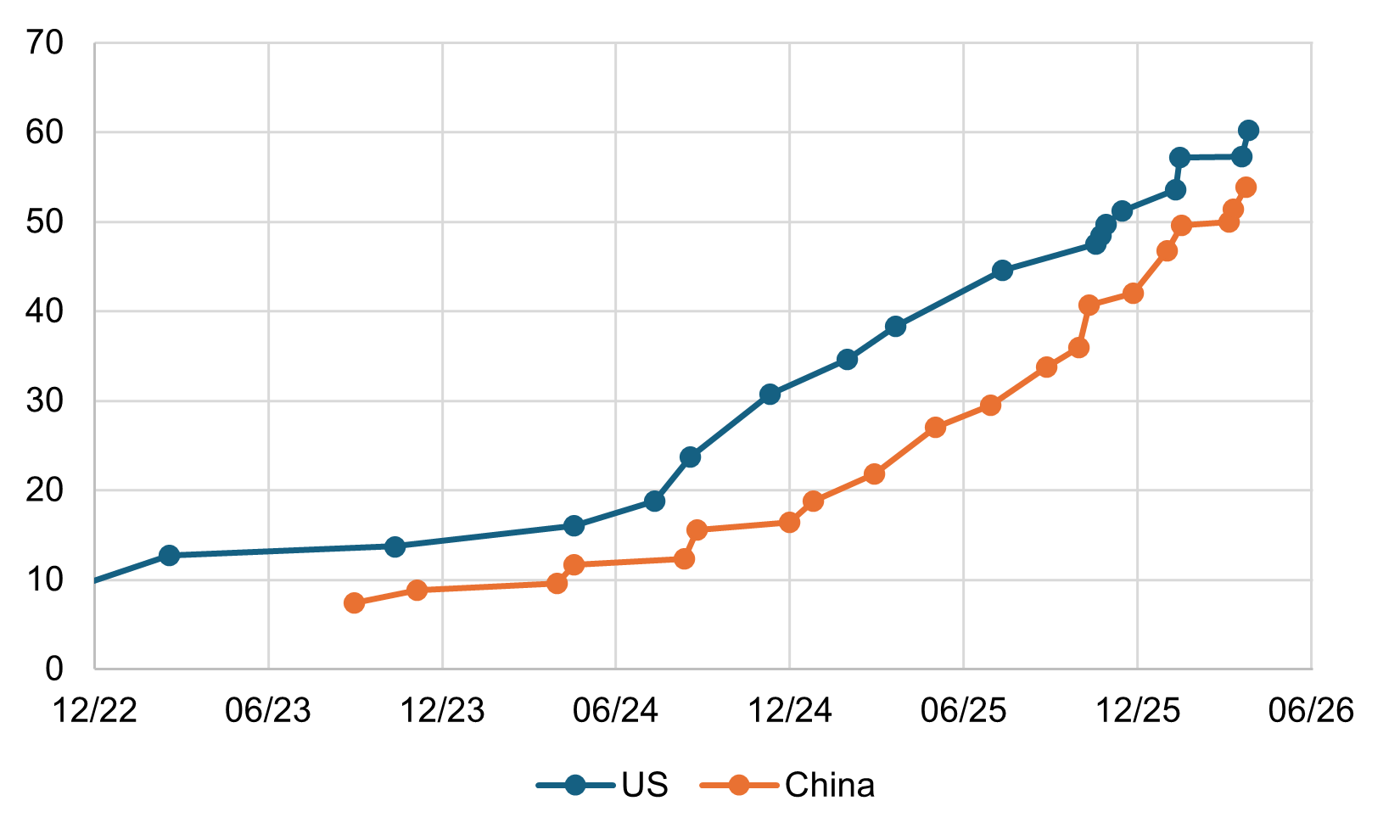

Beyond energy, we see demand for digital infrastructure remaining strong. Demand for AI compute capacity continues to outpace available supply as large technology firms press ahead with substantial capital expenditure plans. While development costs may rise, we believe the structural growth story for data centers and related infrastructure remains intact.

Figure 2: GenAI Model Performance

Source: Artificial Analysis. Data as of April 2026.

Source: Artificial Analysis. Data as of April 2026.

Real estate: Focus on income

Direct real estate began the year with solid momentum. While we believe rising market interest rates present downside risks to capital values, we’ve seen direct real estate proving less sensitive than listed real estate investment trusts (REITs), with many parts of the market helped by higher starting yields following the 2022 repricing.

Forecasting has, however, become challenging in this uncertain environment, making scenario‑based analysis more appropriate, in our view, than point forecasts. An upside scenario—involving limited economic scarring and a return to relative stability—remains possible, though it is increasingly time‑dependent. Conversely, we believe a stagflationary outcome has become more plausible, particularly given elevated energy prices, although is not a base case.

Real estate’s resilience lies in its operational flexibility. Active asset management of both income and physical specification provides potentially valuable levers. We also see location quality and operator selection becoming increasingly critical, particularly in sectors where rising costs can be passed through efficiently to end‑users.

One additional factor is supply. Construction viability may deteriorate as material and energy costs rise. While this poses challenges for developers, it also reinforces structural undersupply of high‑quality stock, which has the potential to underpin rental growth in the medium term.

The takeaway

Private markets are navigating a more volatile and geopolitically charged world, but we believe they are doing so from a position of relative strength. Across credit, infrastructure and real estate, fundamentals remain largely sound, even as risks become more asymmetric and outcomes more dispersed.

Lushan Sun, Head of Cross-Asset Research, Private Markets, with L&G’s asset management business in the UK (Asset Management, L&G); Bill Page, Head of Real Estate Research, Private Markets, Asset Management, L&G; and Dr. James Tyrrell, Private Markets Research Analyst with Asset Management, L&G, authored this blog.

1. Source: Cliffwater, 2026.

2. Source: Cliffwater and JPMorgan, as of 2026.

3. Source: Infralogic, as of April 2026.

4. Source: MSCI, 2026.

Disclosures

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) and Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. Legal & General Investment Management America, Inc. does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that LGIM America's investment or risk management processes will be successful.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.