Hedge when you can, not when you need to

A menu of equity hedging strategies to help defined benefit plans potentially lock in gains and shape outcomes.

After one of the stronger runs equity markets have seen in years, many defined benefit plans find themselves in an enviable spot: gains are on the books and funded status has improved.

But consider the old-time adage on insurance: The best time to think about it is precisely when you feel you need it least. When markets are calm and rising, protection is available and affordable. When markets are falling and everyone wants protection at once, it is expensive and, in the worst moments, hard to come by, not to mention with an unknown amount of the damage already wrought. That is the whole idea behind a simple piece of advice we keep coming back to with clients: Hedge when you can, not when you need to.

This is not a market call. We are not here to tell you equities are about to roll over. It is fair to note that a lot of recent performance has been concentrated, and that parts of the market look more speculative than others. This is worthwhile context. But the case for thinking about protection today does not rest on predicting a downturn. It rests on a simpler idea: When you are ahead, it can make sense to take some uncertainty off the table.

A word on "cost"

When hedging comes up, the conversation often gets pulled into whether volatility is "rich" or "cheap." We would gently steer you away from that framing. These are relative terms, and they can mean different things depending on who is using them and to what ends.

What actually matters to a plan is much more practical:

- The absolute premium - what does this cost me upfront?

- The shape of the outcome - where does my protection start, end and am I giving up upside to get it?

Those questions, set against your plan's funded status, glide path, liabilities and cash flow needs, are what should drive the decision. Every plan has its own starting point, timeline and definition of a good outcome. The right hedge is the one that fits that path, not the one that scores best on a pricing screen.

The menu of equity hedging strategies

Think of what follows as a menu rather than a single recommendation. Most of these strategies are built from just two simple building blocks—the right to sell the market at a set level (a put) and the right to buy it at a set level (a call). Combining them in different ways lets you dial the trade-off between cost and protection up or down to suit your plan.

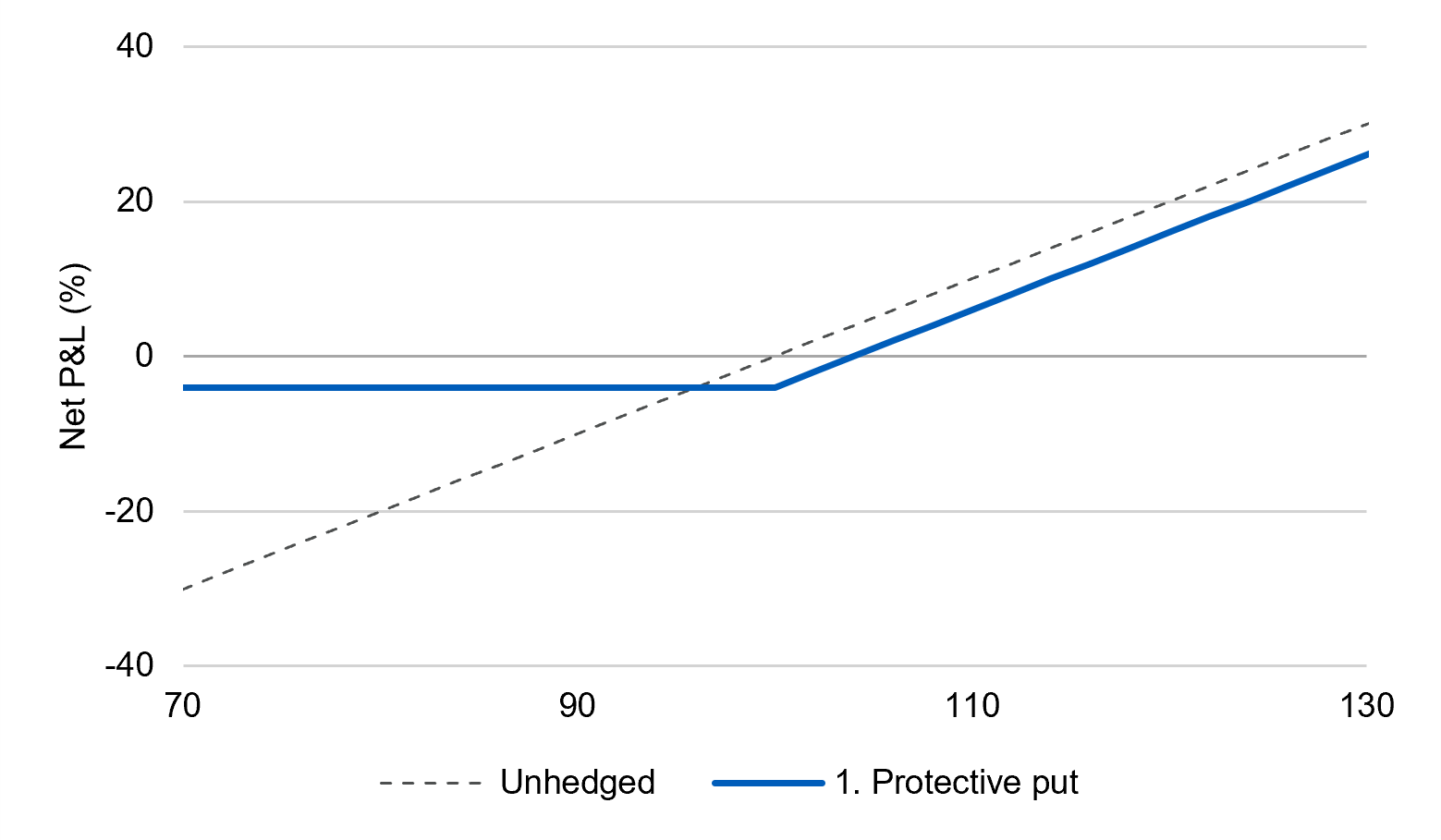

1. Buy protection outright and keep all your upside

The most straightforward choice is to buy a put. Think of it like insurance on your house: You pay a premium, and in exchange you are protected if the market falls below a level you choose. Crucially, you keep all the upside if markets keep rising.

You also get to choose where the protection kicks in. A popular choice is to protect from this year's starting level—in other words, to lock in the gains you have made so far this year. Another common choice is to set the protection a bit below today's market, say 10% lower, respective of returns expectations and accrued levels.

Best for: plans that want to keep full upside and are willing to pay a premium for clean, simple protection.

Figure 1: Protective put

Source: L&G – Asset Management, America. For illustrative purposes only. The illustrative scenario assumes a spot start level of 100, a protective put strike of 100, a protective put premium of 4, and shows the net profit and loss (%) at various index levels.

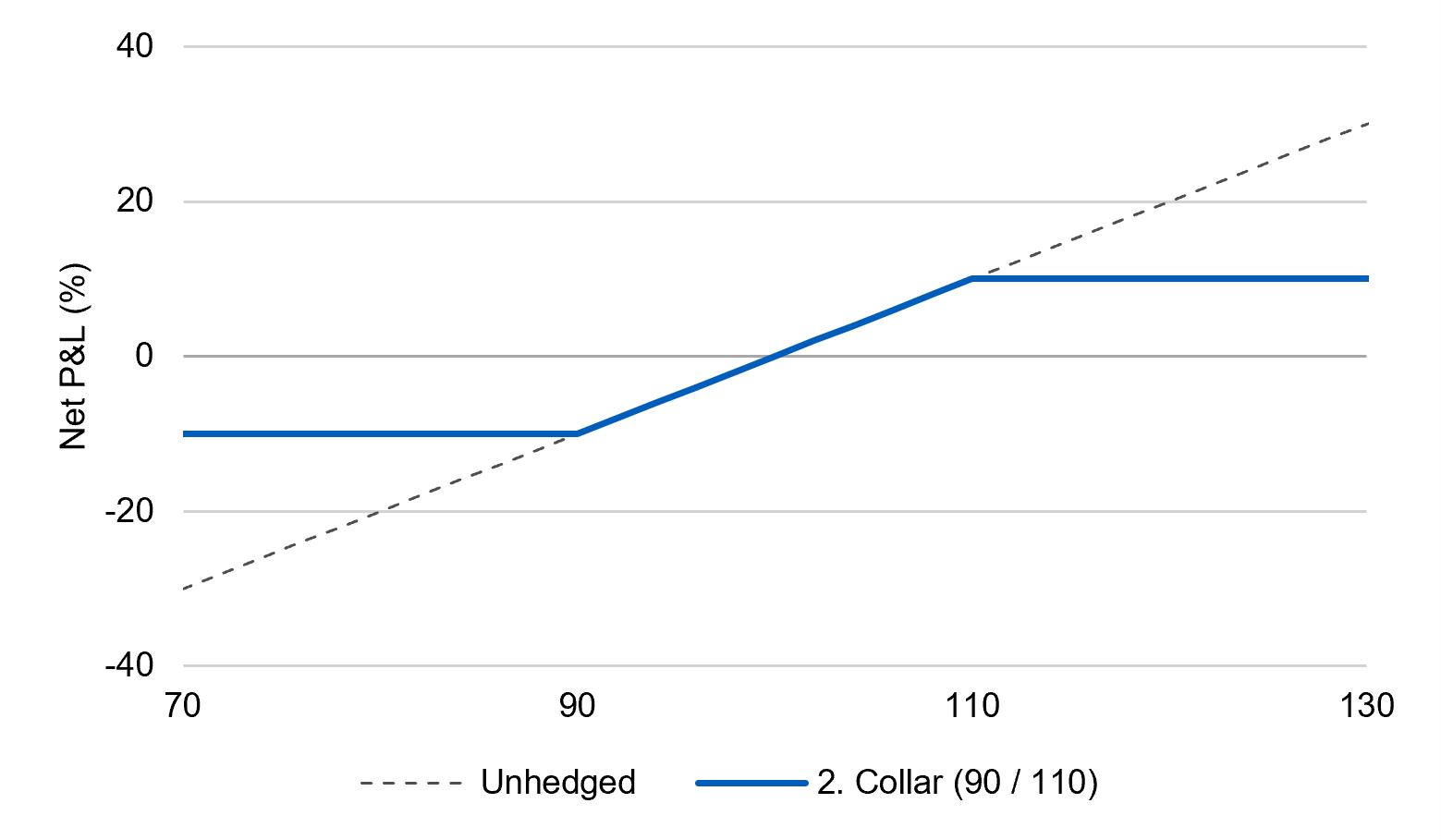

2. Lower the cost with a collar

If paying the full premium is unappealing, you can fund some or all of it by giving up a slice of future upside. This risk management overlay is more focused on shaping outcomes than the premium spent. You buy a put for protection and sell a call to help pay for it. A typical example protects you if the market falls more than 10% and caps your gains beyond about 10%, i.e., a "90 / 110" collar. These can often be structured at little or no upfront cost.

Best for: cost-conscious plans comfortable trading away some of the upside they may not need in order to fund protection.

Figure 2: Collar (90 / 110)

Source: L&G – Asset Management, America. For illustrative purposes only. The illustrative scenario assumes a spot start level of 100, a collar put strike of 90, a collar call strike of 110, a collar net premium of 0, and shows the net profit and loss (%) at various index levels.

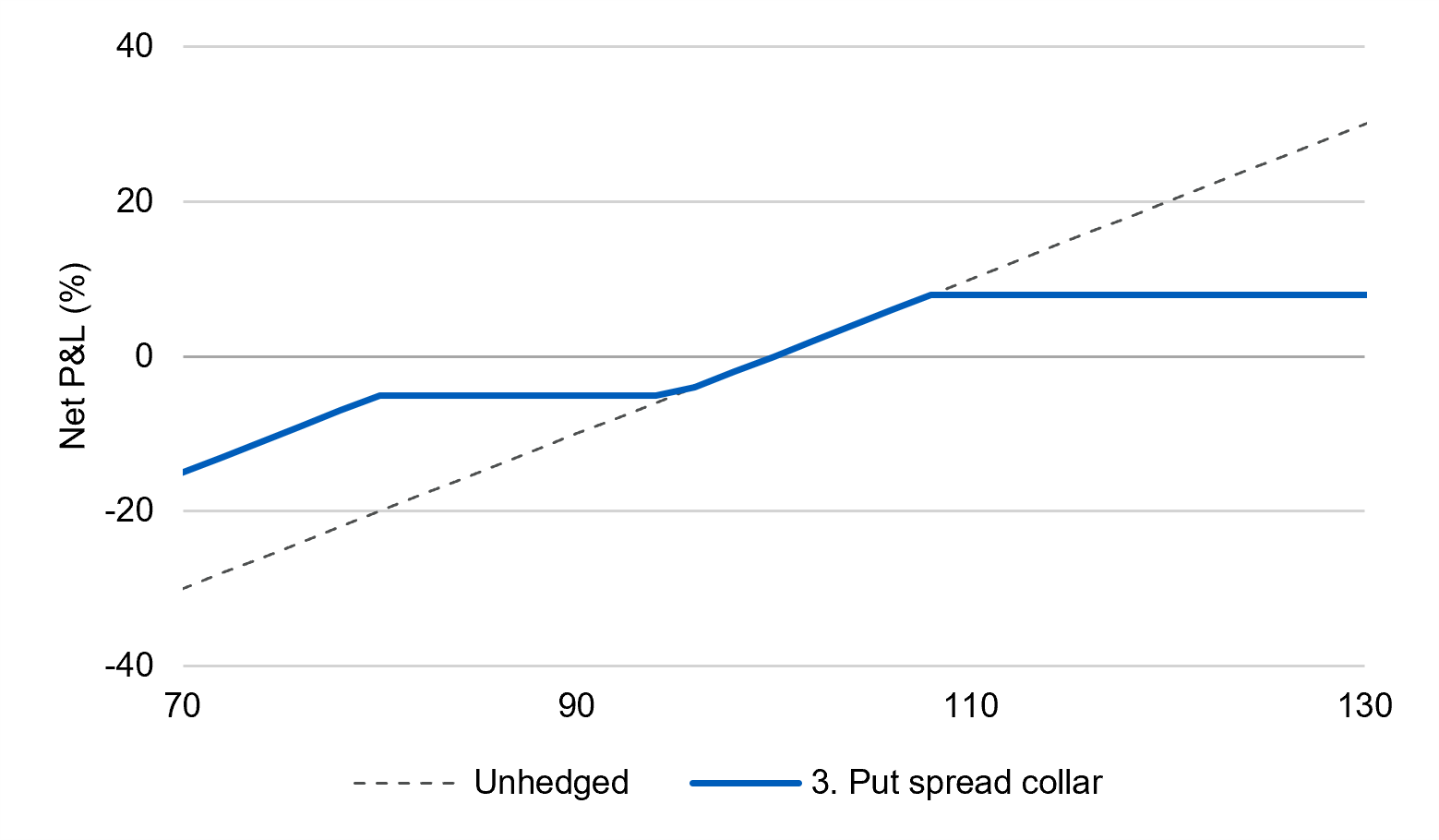

3. The put spread collar, a narrowed trade-off

For plans that want the lowest upfront cost and a more measured near-term posture, a put spread collar is a long-standing pension tool. It works like a collar, but the downside protection covers a defined band, typically anchored more near-the-money for immediacy of loss mitigation. That typically makes it cheaper than the vanilla collar and therefore lets you keep more upside.

Best for: plans focused on the near term that want maximum cost efficiency and accept a defined protection band.

Figure 3: Put spread collar

Source: L&G – Asset Management, America. For illustrative purposes only. The illustrative scenario assumes a spot start level of 100, a put spread collar-long put strike of 95, a put spread collar-short put strike of 80, a put spread collar-short call strike of 108, a put spread collar–net premium of 0, and shows the net profit and loss (%) at various index levels.

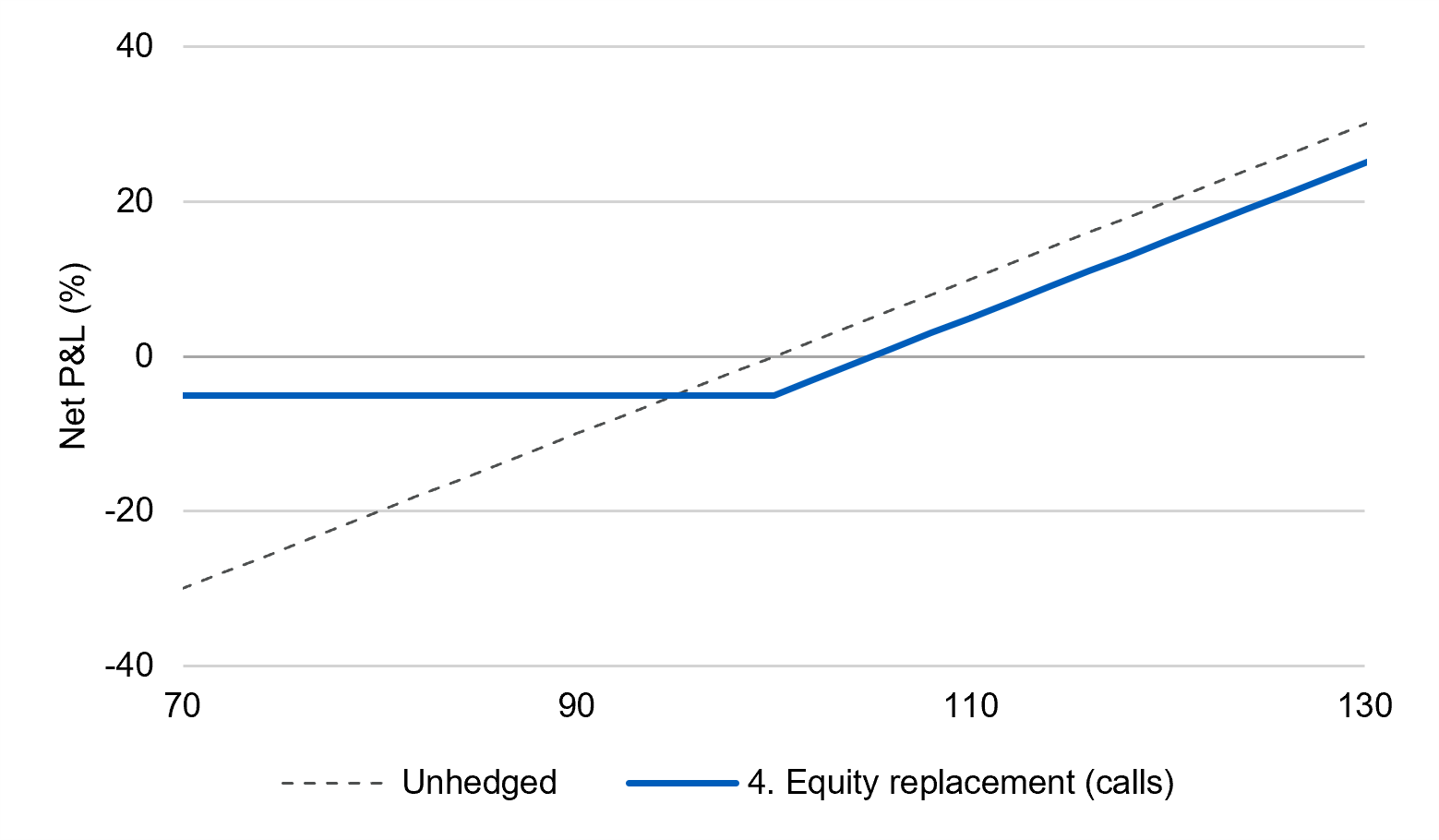

4. Replace equity with calls

The menu is not only about protecting what you own. If you are adding new exposure or want to convert an existing position into something with a defined downside, you can buy a call instead of holding the stock outright. This equity replacement lets you participate in the upside while limiting what is at risk to the premium you paid.

Best for: plans putting new money to work or reshaping existing exposure with a built-in floor.

Figure 4: Equity replacement (calls)

Source: L&G – Asset Management, America. For illustrative purposes only. The illustrative scenario assumes a spot start level of 100, an equity replacement-call strike of 100, an equity replacement-call premium of 5, a payoff convention net of premium, and shows the net profit and loss (%) at various index levels.

How long should a hedge last?

Most strategic hedges sit in a 6–12-month window, a horizon that is long enough to ride out a typical bout of turbulence without constantly rolling positions. It is also structurally compatible with institutional decision-making horizons.

If you are not ready to commit to a longer plan, a shorter 3–6-month hedge can act as a bridge: It covers near-term tail risk while you and your team work through the bigger-picture decisions. There is no need to solve everything at once.

Why index options look especially attractive right now

Concentration keeps coming up in our conversations. Plans aren't worried about the average stock so much as the reality that a handful of large names have driven much of the gain and could pull the market down together if the mood shifts.

A broad index hedge is built for exactly that. Instead of protecting any one position, it protects your whole equity allocation against a market-wide fall: the "everything moves together" scenario that concentration creates.

Yet so much attention is on the seeming speculative forces in a very small group of companies that the larger risk of contagion appears to be overlooked. In simple terms, option prices suggest that market participants are still paying up for protection from swings in specific companies in isolation but not placing the same value on the possibility that many stocks could fall together at once. That mismatch can make index protection look particularly appealing, as it may be cheaper than buying protection on individual stocks.

This is the irony of today’s market. The same concentration that is driving single-stock options prices relatively higher are also the conditions that can lead to a sharp, broad sell-off that an index option can best insure. With the risk of broader contagion underpriced even under current conditions, perhaps this is the right moment to hedge when you can, not when you need to.

Closing thoughts

None of this requires a view that markets are about to fall. It simply recognizes that protection is easiest to arrange from a position of strength.

For more than 20 years, we have taken a holistic approach to managing funded-status risk for pension plans. Across the spectrum, from liability-driven portfolios to designing custom equity hedges, we focus on solutions to meet bespoke objectives. That experience shapes how we think about design, implementation and trade-offs across different market environments.

Today, at the intersection of exceptional recent market returns, concentration concerns, and relatively favorable options pricing, we believe now may be the time to consider an equity hedge.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.

Disclosures

Unless otherwise stated, references herein to "L&G" and “L&G – Asset Management” refer to the global asset management business of Legal & General Group plc. that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser), Legal & General Investment Management Japan KK (licensed by the FAS in Japan), and LGIM Singapore Pte. Ltd. (licensed by the MAS in Singapore). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. L&G – Asset Management, America does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that L&G – Asset Management, America’s investment or risk management processes will be successful.