A Cash Balance Plan Hedging Playbook

The prevailing institutional industry narrative has long centered on the steady decline of corporate defined benefit (DB) plans as companies switch to defined contribution (DC) plans. Although the DB sector still represents roughly $3 trillion in assets, its growth continues to lag other institutional channels. However, one segment of the DB sector is expanding rapidly: cash balance plans. Between 2001 and 2020, the number of cash balance plans increased more than fifteen-fold, rising from about 3% of all DB plans to nearly 50%.1

A cash balance plan can be thought of as a hybrid defined benefit (DB) plan that includes elements similar to a DC plan, such as tax-deferred savings and high-contribution limits. Its defined benefit is a stated account balance, with the employer making tax-deductible employer contributions and bearing the investment risk. In a typical cash balance plan, a participant's account is credited annually with a "pay credit" (e.g., a set percentage of compensation) and an "interest credit" (either a fixed rate or a variable rate linked to a Treasury yield or a return on plan assets).

A distinct challenge

Hedging the liability profile of cash balance plans with interest crediting rates tied to a Treasury yield, particularly those that incorporate a minimum floor, presents a distinct challenge.

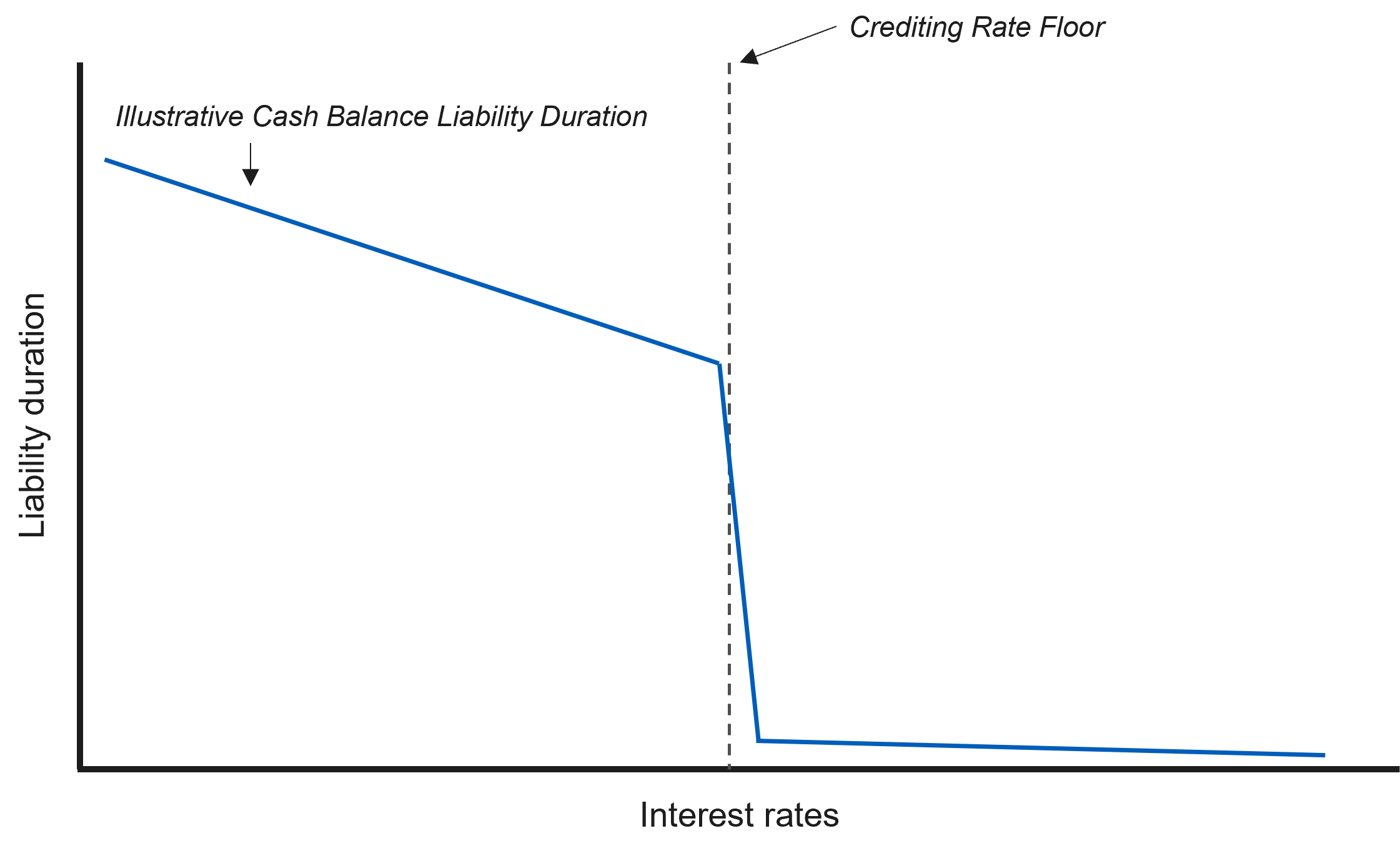

By offering participants an interest crediting rate linked to, for example, the 30year Treasury yield subject to a 4.5% floor, the plan sponsor has effectively granted a free option. While this feature can be a valuable tool for employee recruitment and retention, it introduces a liability pattern that traditional fixed income instruments cannot fully replicate. As illustrated in Figure 1, the presence of a floor prevents any conventional bond portfolio from matching the full range of potential liability movements.

Figure 1: A liability pattern that traditional fixed income instruments cannot fully replicate

Source: L&G – Asset Management, America. For illustrative purposes only.

Source: L&G – Asset Management, America. For illustrative purposes only.

In a simplistic scenario, the liability duration will be close to zero when rates are above the floor and will be closer to a traditional liability duration (e.g., 9-12 years) when rates are below the floor. The drastic shift in duration when rates breach the floor is challenging to hedge, especially without the use of derivatives.

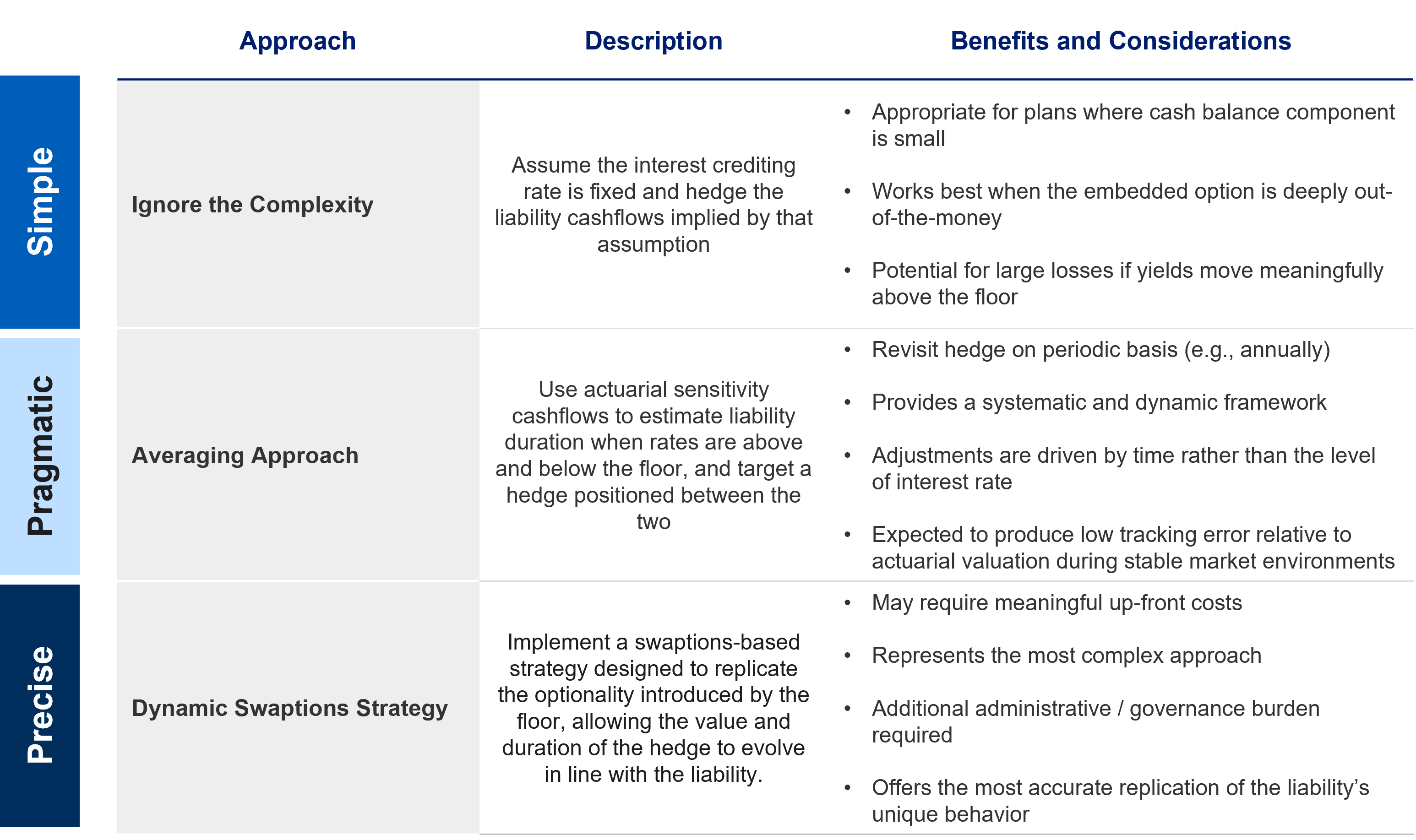

Approaches to this dynamic range from the simple to the pragmatic to the precise. Although there is no silver bullet, we believe our experience working with cash balance plan sponsors provides a clear framework for evaluating the available approaches. We find that each alternative carries tradeoffs, and the optimal strategy depends on the sponsor’s risk tolerance, plan design and broader investment objectives. Figure 2 illustrates this framework in more detail.

Figure 2: A framework for evaluating available approaches

Source: L&G – Asset Management, America. For illustrative purposes only.

It is important to acknowledge that no market instrument perfectly hedges the exposures created by a floorbased interest crediting rate. The goal, therefore, is to select an investment approach that most effectively manages a plan’s unique risks while aligning with the sponsor’s overall objectives.

1. Source: What Are Cash Balance Plans? Tax Policy Center, https://taxpolicycenter.org/briefing-book/what-are-cash-balance-plans

Disclosures

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes Legal & General Investment Management Ltd. (a U.K. FCA authorized adviser), Legal & General Investment Management America, Inc. (a U.S. SEC registered investment adviser) and Legal & General Investment Management Asia Limited (a Hong Kong SFC registered adviser). The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of the date set forth above and may change based on market and other conditions. The material may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. Legal & General Investment Management America, Inc. does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that LGIM America's investment or risk management processes will be successful.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.